Drift Myth and The Influence of Active Management on Morningstar’s Style Box

FEBRUARY 2024

When it comes to investing, few things are certain. That reality is one reason why investors rightly want their portfolio allocations to follow predictable and stable investment mandates—after all, a value fund should act like a value fund. For investors seeking pure beta, myriad options of passive strategies can reliably deliver the desired exposure across a wide range of categories. But when it comes to active strategies designed to outperform a benchmark—which, by definition, means frequently deviating from a benchmark—how can investors be confident they’re getting what they intended?

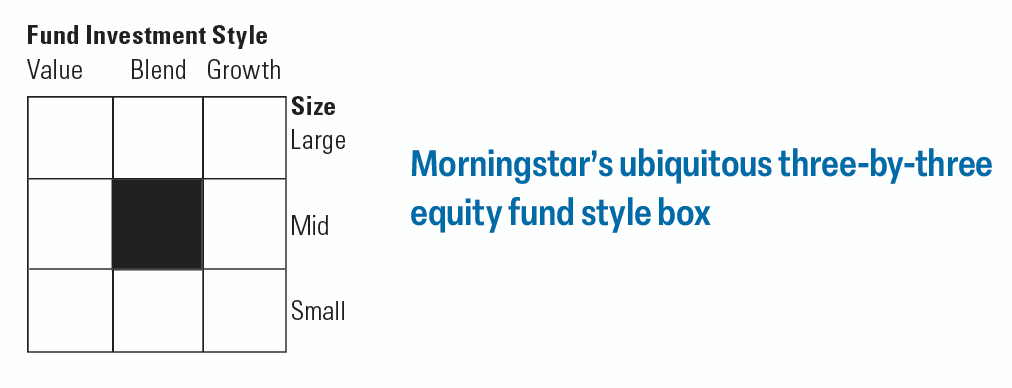

One industry standard for getting a better read on how a fund is invested is to use Morningstar’s style boxes. These nine-square grids plot where an equity fund sits with regard to market capitalization (small-, mid-, and large-cap) relative to its investment style (growth on the right side of the grid, value on the left, and blend in the middle). Morningstar also tracks how a fund has invested across those nine segments over the trailing five years, which can offer a useful point of comparison in seeing how a fund’s current weightings stack up with its typical allocations. But before drawing any conclusions, it’s important to understand how Morningstar makes its calculations.

Why a fund’s Morningstar category and investment style can sometimes diverge

Determining a fund’s investment style begins with some quantitative screening. Morningstar looks at each holding in a portfolio at a point in time and assigns it a value score, which it then subtracts from the holding’s growth score. Each of those net scores is weighted proportionally and the result is the fund’s overall style score. Lower scores for a fund indicate a strong value tilt, while higher scores reflect a bias toward growth. The individual metrics used to determine these value and growth scores are quite different, however, and worth a closer look.

While both scores take into account historical and forward-looking measures, only Morningstar’s value score factors in familiar valuation metrics, including price-to- earnings and price-to-book ratios, as well as dividend yield. The growth score, meanwhile, parses an entirely different data set that includes earnings, sales, and cashflow growth. As a result, it’s not accurate to say securities that rank strongly in Morningstar’s value metrics are the cheapest stocks on the market, while growth stocks are the most expensive. The reality is far more nuanced than that—and more fluid. Where Morningstar draws the line between value, core, and growth varies over time depending to some degree on larger market forces, but in general each style category will account for roughly one-third of the total market float.

This process is distinct from Morningstar’s fund category assignments, which is a much slower moving, qualitative undertaking. These category labels are designed to help communicate a fund’s general investment approach, and also to defi ne the fund’s peer group, which ideally consists of funds with similar mandates and investment criteria. Currently, Morningstar tracks more than 100 unique fund categories spread over nine broad category groups (U.S. equity, taxable bond, etc.). Those category assignments are initially based on each fund’s trailing three-year portfolio statistics— as defined by Morningstar—but are also subject to editorial review and approval.

This process is distinct from Morningstar’s fund category assignments, which is a much slower moving, qualitative undertaking. These category labels are designed to help communicate a fund’s general investment approach, and also to defi ne the fund’s peer group, which ideally consists of funds with similar mandates and investment criteria. Currently, Morningstar tracks more than 100 unique fund categories spread over nine broad category groups (U.S. equity, taxable bond, etc.). Those category assignments are initially based on each fund’s trailing three-year portfolio statistics— as defined by Morningstar—but are also subject to editorial review and approval.

Large Cap Value

Our flagship U.S. equity strategy targeting attractively valued large-cap companies.

Twice a year, Morningstar reviews its category assignments and makes any necessary adjustments if analysts believe a fund has changed its investment approach. Category reassignments aren’t common, but they do happen—and usually indicate that some material change to a manager’s process has taken place.

The key takeaway here is that any given stock can and will see its style score change over time, sometimes dramatically, as its price and fundamentals fluctuate, not to mention the shifting boundaries that separate Morningstar’s broad style buckets. Those fluctuations mean that a fund with a clearly defined growth- or value-oriented investment approach (reflected in a corresponding Morningstar category assignment) can often drift into “blend” territory within the style boxes as market conditions change.

A short-term change in style can be the result of disciplined active management

Persistent deviations from a fund’s Morningstar category are sometimes referred to as “style drift”—for example, when a mid-cap fund begins holding more and more large cap names, or a value manager makes a habit of owning growth stocks. But there’s a big difference between meaningful style drift that results from a portfolio manager having loose investment standards and the apparent shifts in style that may result from a manager actively targeting opportunities.

At Boston Partners, we’re value managers, first and foremost: Finding attractively valued opportunities is a foundational part of our three-circle stock-selection process. But we seek out securities that also offer strong fundamentals and positive business momentum in addition to being reasonably valued. What that means in practice is that we can, and often will, hold stocks in our portfolios that can rank highly for Morningstar’s value scores, or occasionally its growth scores—or both.

Halliburton is one example. Before the pandemic struck in 2020, the energy industry was still working through the effects of a fairly dramatic collapse in energy prices coupled with an oversupplied market, particularly in North America, where investment in fracking had been accelerating. Then in the first half of 2020, the stock plummeted to levels not seen in more than 30 years. We thought the stock was clearly attractive from a valuation perspective, and the consensus expectations for its future growth at that time were unreasonably bearish for a company with such solid fundamentals. Lastly, we also saw a catalyst for change emerging, given the increasing consolidation in the industry, especially in the oilfield service space. Halliburton was a stock that met all three of our broad investment criteria, and one that we were able to purchase at a steep discount to intrinsic value; as of this writing, we continue to hold it in several of our portfolios. Yet Morningstar currently classifies Halliburton as a growth stock, in large part because of how dramatically its business momentum improved relative to unusually low points of comparison set during the pandemic.

Another point worth considering: Morningstar’s value score is the only one that considers price, which is often the most rapidly changing metric in the stock market. A company’s projected earnings (a factor in the growth score) may not meaningfully change from one quarter to the next, but its price certainly can, which in turn affects the value score it receives. The bottom line is that stocks with strong value characteristics may not retain them for very long. Active value managers like us often need to act quickly to capture those opportunities when they arise.

Style boxes are a useful guide, but far from definitive

At Boston Partners, we believe the best investor is an educated one, so we’ve long been proponents of transparency when it comes to our portfolios and process. To that end, we believe Morningstar’s style boxes are a valuable tool for understanding more about the types of securities a fund targets, how wide a net it casts, and how consistent it’s been over time. But it’s important for investors to know that the delineation between styles is often fluid, and the variables that dictate an individual security’s classification can change quickly and dramatically—especially in volatile markets. One thing that is certain, in any kind of market, is our commitment to our time-tested process of seeking out securities trading at an attractive valuation, with strong business fundamentals, and positive business momentum—characteristics that, in our experience, tend to drive outperformance over time.

About Boston Partners

Boston Partners is a value equity manager with a distinctive approach to investing— one that combines attractive valuation characteristics with strong business fundamentals and positive business momentum in every portfolio. The consistent application of this approach over nearly 30 years by an experienced and long-tenured team has created a proven record of performance across economic cycles, market capitalizations, and geographies.

Important Disclosure Information

The opinions expressed are those of the contributors as of February 2024 and are subject to change. No forecasts are guaranteed. This commentary is provided for informational purposes only and is not an endorsement of any security, mutual fund, sector, or index. Boston Partners and affiliates, employees, and clients may hold or trade the securities mentioned in this commentary. Past performance does not guarantee future results.

Stocks and bonds can decline due to adverse issuer, market, regulatory, or economic developments; foreign investing, especially in emerging markets, has additional risks, such as currency and market volatility and political and social instability; value stocks may decline in price; growth stocks may be more susceptible to earnings disappointments; the securities of small companies are subject to higher volatility than those of larger, more established companies. This material is not intended to be, nor shall it be interpreted or construed as, a recommendation or providing advice, impartial or otherwise. Beta is the return generated from a portfolio that can be attributed to overall market returns. Intrinsic value is a measure of what an asset is worth, which may differ from its current market price.

Boston Partners Global Investors, Inc. (Boston Partners) is an Investment Adviser registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940. Registration does not imply a certain level of skill or training. Boston Partners is an indirect, wholly owned subsidiary of ORIX Corporation of Japan. Boston Partners updated its firm description as of November 2018 to reflect changes in its divisional structure. Boston Partners is comprised of two divisions, Boston Partners and Weiss, Peck & Greer Partners.

Securities offered through Boston Partners Securities, LLC, an affiliate of Boston Partners.